en

en  Italian

Italian French

French German

German Spanish

Spanish Portuguese

Portuguese

- 14/07/2025

- Economy and marketing

Exports in the wood-furniture sector closed the first quarter of 2025 stable at €4.7 billion, down 0.4% overall compared to the same period in 2024.

This is what emerges from data processed by the FederlegnoArredo Study Center based on Istat data, which provide a snapshot of exports in the first quarter of a sector waiting to see what will really happen in terms of tariffs and what path Trump intends to take.

EU27 area is the leading market

The leading market for our exports remains the EU27 area with €2.5 billion, down 0.2%, while exports to non-EU27 countries grew by 1.7% to €690 million.

The furniture macro-system recorded a -1.1% decline with €3.4 billion in exports: the greatest slowdown was seen in kitchens (-8.3%) and office furniture (-9.8%). The wood macro-system, on the other hand, grew by +1.6% to a value of €1.25 billion, thanks to the good performance (+9.7%) of furniture products and finishes for the construction industry.

Some positive signs

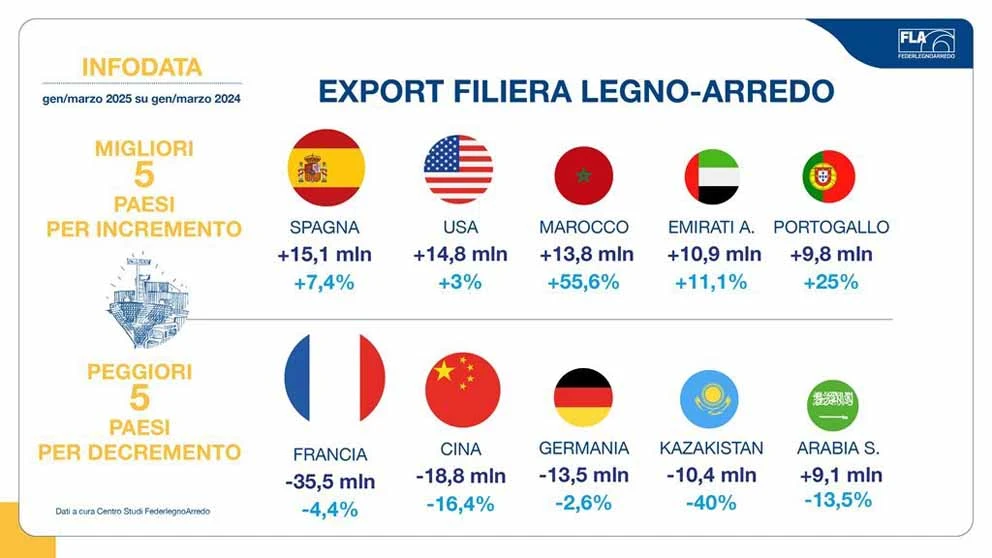

There are some positive signs for the supply chain from non-EU markets, particularly from the US, which recorded a +3% increase in the January-March period after a -0.1% decline in January-February. This may be due to attempts to anticipate the application of the tariffs announced by Trump, who moved the deadline from July 9 to August 1. The UK and the United Arab Emirates also confirmed their dynamism in the first months of 2025, while, on the EU market, Spain and Portugal stood out with growth figures.

As far as imports are concerned, China stands out with a figure of +25% (March 2025 compared to March 2024), while the cumulative figure for the quarter reached +38.2%.

Impossible to imagine the future

Commenting on the data, FederlegnoArredo president Claudio Feltrin reiterates how, for almost a year now, it has been truly impossible to imagine even the immediate future for a number of very complex reasons. Not only that, but while we are at the mercy of the US president's statements, the negative trend in the main countries that import our products also continues.

In fact, France and Germany continue to decline in the Top 10 (-4.2% and -2.6% respectively), while the UK and Spain recorded +3.3% and +7.4%; the United Arab Emirates recorded the best percentage change with +11.1% for a total export value of €108 million.

The figure for imports of Chinese products into Italy, which reached +25% in March, may be a warning sign, even though Istat data for April 2025 show a 3.5% decline in imports for furniture.

Business confidence down

The five countries with the highest growth in absolute terms in January-March 2025 are, in addition to Spain, the US, and the UAE, Morocco +55.6% (26th destination) and Portugal +25% (21st destination). Among the five countries with the worst negative trends are France and Germany, which lost €35.5 million and €13.5 million respectively in the Top 10; China (12th destination) recorded a decline of 16.4% and Saudi Arabia of 13.5% (16th destination).

"A small positive sign? - concludes Feltrin - We will find out in the coming months, but the advance of the Chinese giant should not make us too complacent. It is no coincidence that, given the climate of confidence expressed by companies in May, the balance of opinions on orders (the difference between opinions on high and low orders) stands at -24.1%, down from -20.2% in April. At the same time, it should be noted that 61.7% of companies still report that orders are ‘normal’, in line with expectations: this is also confirmed by industrial furniture production, which recorded a +5.4% increase in the period January-April 2025."