en

en  Italian

Italian French

French German

German Spanish

Spanish Portuguese

Portuguese

- 16/04/2026

- Economy and marketing

The data on furniture exports for January 2026 processed by the FederlegnoArredo Study Center, based on Istat sources, reveal a complex picture for the wood-furniture sector, highlighting a phase of strong slowdown, a widespread weakness of international demand, with some areas that nevertheless show greater resilience.

As for industrial production in manufacturing, February recorded +0.9% and for the two-month period -0.5%, in line with that of furniture which is essentially stationary (-0.5% in February and -0.6% the cumulative two-month figure).

Negative trend for exports in January 2026

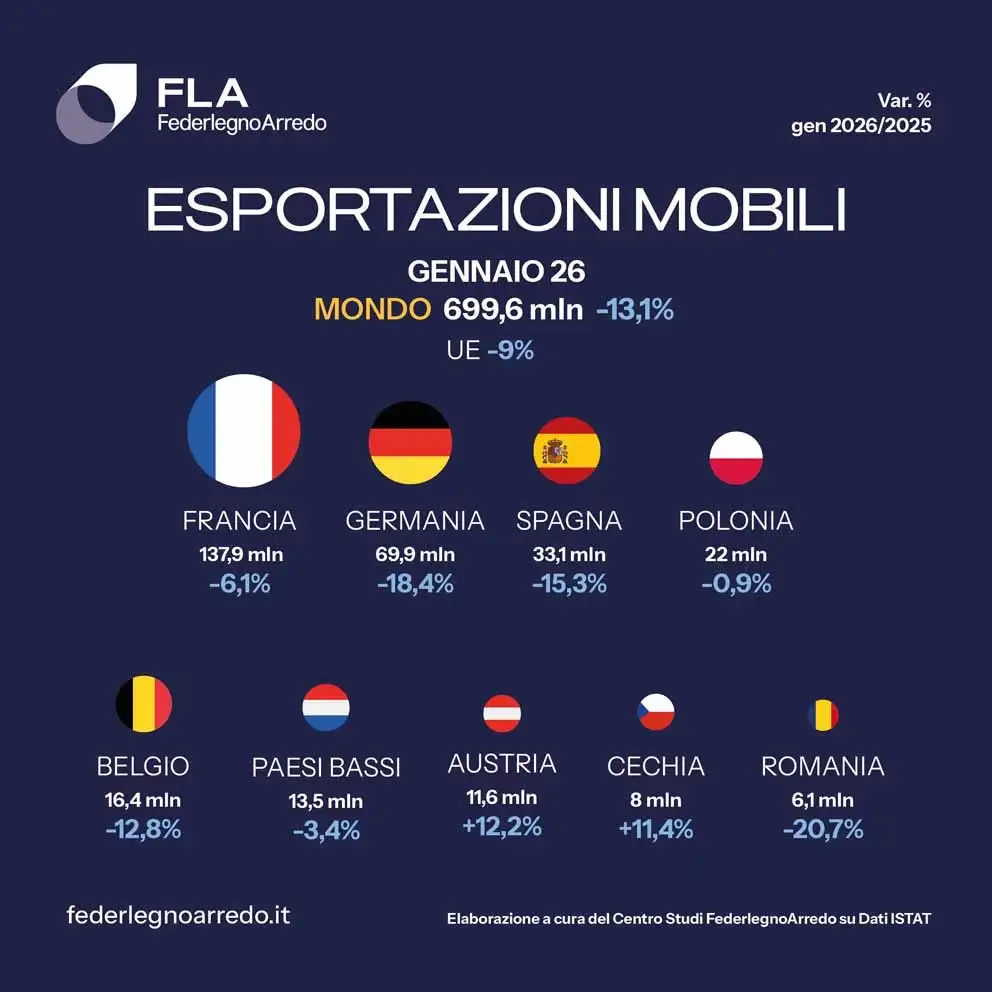

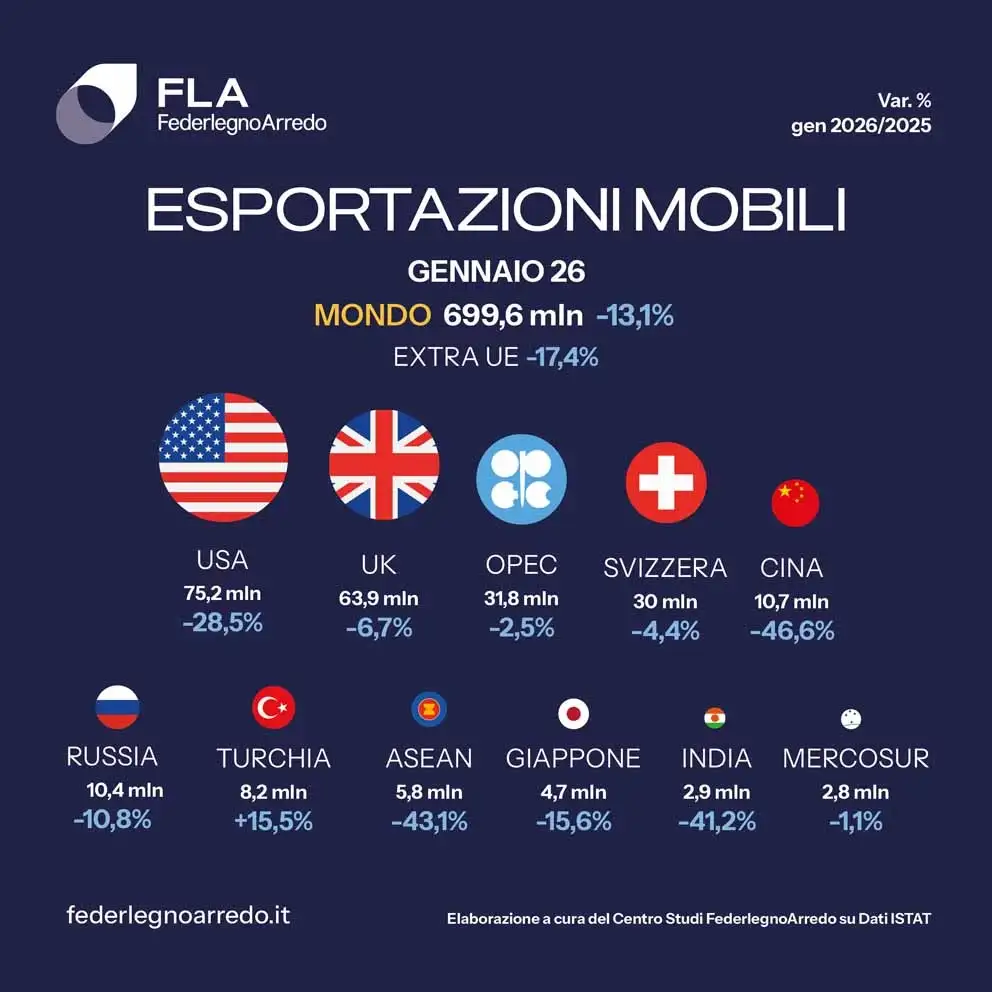

In January Italian furniture exports worldwide, amounting to about 700 million euros, fell by 13.1%, with a widespread decline both in European markets (-9%) and in non-EU markets (-17.4%). The contraction toward the United States is particularly significant, reaching -28.5%; France -6.1%; Germany -18.4%; Spain -15.3%; the Netherlands -3.4%; the United Kingdom -6.7% and China -46.6%. The OPEC countries recorded -2.5%. Only two positive signs, those of Austria (+12.2%) and the Czech Republic (+11.4%), whose volumes are however still too small to be decisive in the overall scenario.

Strengthening the international presence of companies

The 2025 final accounts had shown how the wood-furniture supply chain recorded a slightly increased turnover (+1.4%), supported by the domestic market amounting to 33 billion euros (+2%) and exports that had remained virtually stable (+0.4%).

“Our companies – explains the president of FederlegnoArredo, Claudio Feltrin – now must try to defend this far from guaranteed result, even though they, once again, find themselves managing a complex and unpredictable situation. Covid first, the war in Ukraine, US tariffs, the war in the Middle East and rising energy costs.

The ability of our industry to react has been severely tested in recent years, but the responses have not been long in coming. Now it is even more necessary to strengthen companies' international presence, accompanying them more decisively in diversification processes toward new high-potential markets.”

There are some signs of improvement in business confidence: for example, the balance of opinions on orders expressed in March 2026, while remaining negative, improved by over 13 percentage points after the first two months of 2026.

Salone del Mobile.Milano: an indispensable event

The competitiveness of the supply chain is seen above all in the ability to create a system: companies and institutions must move together to consolidate the international positioning of Made in Italy, also defending it from increasingly widespread unfair competition.

One element to monitor concerns the global trade dynamics induced by US tariffs. In 2025 the European Union recorded an increase in imports from China in the wood-furniture supply chain of 1.3%, compared with a reduction in purchases from other non-EU countries of -1.6%.

“In this context – says Feltrin – the Salone del Mobile.Milano confirms itself as an indispensable event for the entire sector: a concrete and accessible platform also for small and medium-sized enterprises, where they can achieve the best results in direct contact with buyers. The Salone represents a tangible response to the difficulties of the moment: a place where companies can strengthen their positioning and reach new contacts, while at the same time continuing to maintain a presence in traditional markets.”

Australia, a high-potential market

Among emerging opportunities FederlegnoArredo highlights Australia, also in light of the recent free trade agreement signed with the European Union. Under this agreement over 99% of tariffs on European exports to the Australian market will be eliminated, access to critical raw materials will be improved and strategic ties with the Indo-Pacific region strengthened.

Although Italian exports to Australia remain contained (about 180 million euros), there are large margins for growth: the country in fact has high potential, also showing high levels of average wealth, indicative of a broad middle class with significant spending power. It ranks 5th globally for average wealth per adult and 2nd globally for median wealth, second only to Luxembourg (Source: UBS Global Wealth Report 2025). Australia, with 1,904 thousand millionaires, has a very high share of wealthy people relative to the total population (about 7%). All these data indicate widespread prosperity and a less polarized wealth distribution compared with other advanced economies. Finally, growth prospects further strengthen interest in this market: Oceania (in which Australia is the most important country) is among the regions for which sustained growth of average wealth per adult is expected over the next five years, albeit at rates lower than those of the United States and China.